If you’re managing a multi-unit residential building or sitting on a Strata Council in the Lower Mainland, you don’t need me to tell you that the insurance market in British Columbia has been… well, a bit of a rollercoaster. We’ve seen premiums skyrocket and deductibles for water damage climb from a manageable $5,000 to a eye-watering $100,000 or more in some Vancouver high-rises.

It’s a stressful spot to be in. You’re responsible for the building’s assets, the owners’ investments, and a budget that seems to be under constant pressure from rising costs. But here’s the good news: insurance companies aren't just looking to penalize you. They are looking for certainty. Specifically, they want proof that your building isn't a ticking time bomb for water damage.

At Leak Logic Canada, we’ve helped countless property managers across Burnaby, Richmond, and Surrey turn the tables on their insurers. By implementing the right technology and: more importantly: proving its effectiveness, you can negotiate from a position of strength. Here is how you can document and present your risk mitigation strategies to lower those premiums.

Why Do Insurers Care So Much About Water Leaks?

In the B2B world of property management, water is often a bigger threat than fire. A single burst pipe on the 15th floor of a downtown Vancouver condo can cause millions in damages across dozens of units and common areas. This high frequency and high severity of claims are why underwriters are so cautious.

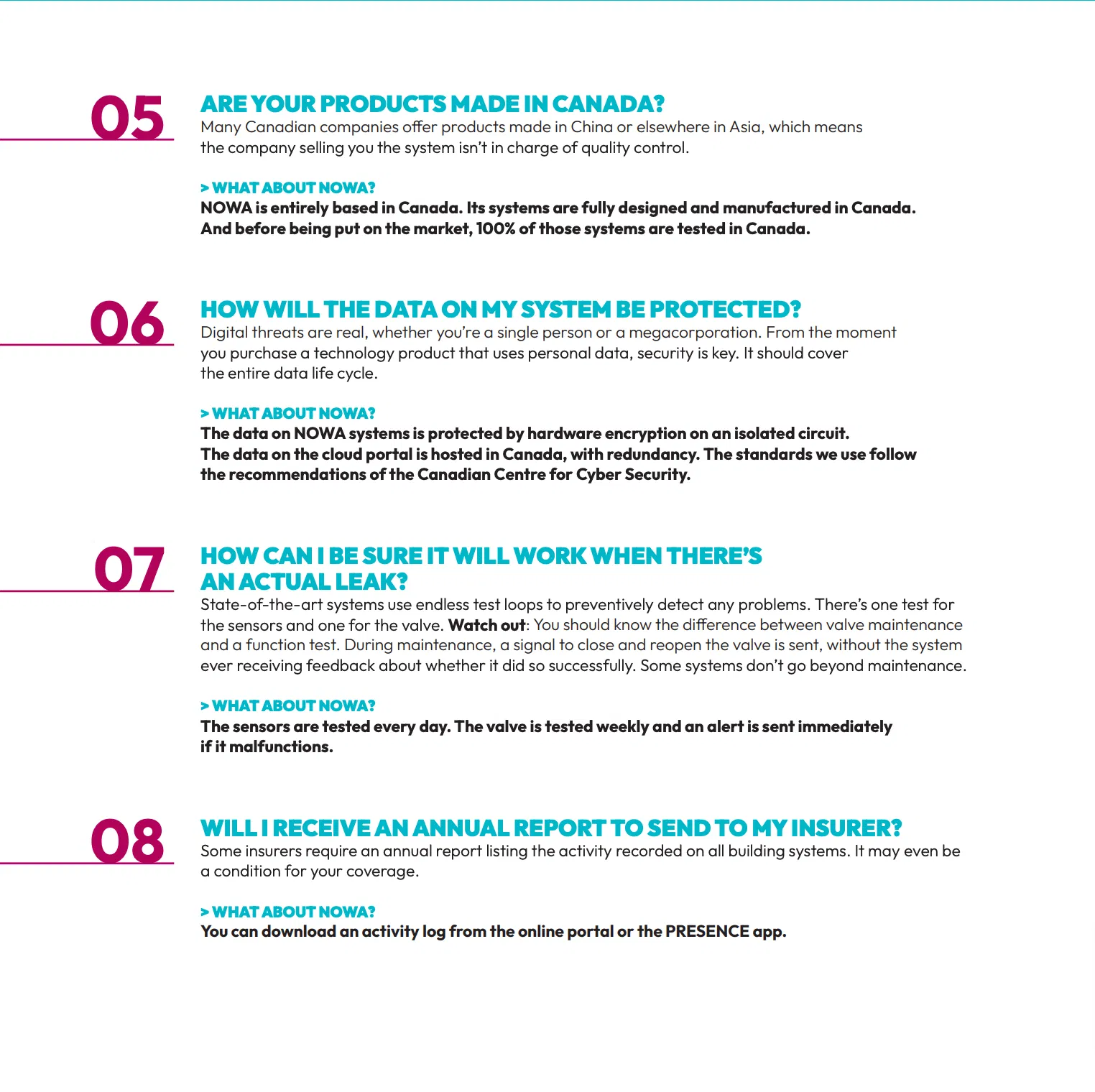

When an insurance company looks at your building, they see a risk profile. If you have no mitigation system in place, they assume the worst: that a leak will go undetected for hours, leading to a massive claim. However, if you can prove that a leak will be detected and stopped in seconds, you change their math.

How Can I Prove My Building is Low Risk to an Underwriter?

Simply telling your broker "we have sensors" isn't enough anymore. To see a real impact on your premiums or deductibles, you need a comprehensive "Proof Portfolio." Think of this as your building’s resume for safety.

1. Highlight the Technical Superiority of the System

Insurers aren't impressed by "smart home" toys. They want commercial-grade reliability. When we install the Nowa system, we emphasize the technical specs that provide maximum protection:

- 0.015-inch Leak Sensitivity: This means the system catches the "weeping" pipe before it becomes a flood.

- Gold-Plated Probes: Unlike cheaper sensors that corrode and fail, gold-plated probes ensure the system works five or ten years down the line.

- 5°C Freeze Alerts: Especially important for buildings in the Lower Mainland during those snap cold fronts, preventing burst pipes before they happen.

- Automatic Water Shut-off: The "hero" of the system. Detection is useless if no one is on-site to turn the valve. Our systems shut the water off at the source instantly.

2. Provide Certification and Compliance Documents

In British Columbia, insurers look for recognized standards. Documentation showing that your system is PREVCAN certified or meets specific insurance compliance standards is vital. This takes the guesswork out of the underwriter's job.

3. Show the Data Protection and Redundancy

Property managers are often concerned about cybersecurity. Your Proof Portfolio should mention that systems like Nowa use hardware encryption and cloud redundancy. This ensures that even if the building's Wi-Fi goes down, the system is still protective. Many of our clients in the Vancouver area opt for LTE-enabled systems to ensure 24/7 connectivity regardless of the local network status.

The Power of 24/7 Monitoring and Reporting

One of the biggest hurdles for property managers is the "after-hours" nightmare. A leak at 2:00 AM on a Sunday is the most expensive kind of leak. When you present your mitigation plan to an insurer, emphasize the PRESENCE service offered by Leak Logic Canada.

This isn't just a local alarm; it’s a dedicated 24/7 remote monitoring service. We see what’s happening in your building in real-time. If a sensor trips, the water shuts off, and the property manager is notified immediately. Providing your insurer with a sample of the monthly reporting: showing that sensors are tested daily and the system is fully operational: is incredibly persuasive. It proves you aren't just "setting and forgetting" your safety equipment.

How to Talk to Your Insurance Broker Before Renewal

Timing is everything. Don't wait until two weeks before your policy expires to mention your new leak detection system. Start the conversation at least 90 days out.

Ask your broker specifically: "What credits or deductible reductions are available if we install a PREVCAN-certified automatic water shut-off system with 24/7 monitoring?"

By asking this early, the broker has time to shop your building to different underwriters. Some carriers, like Northbridge Insurance, even have specific programs (like the Onyx policy) that are designed to reward buildings using advanced leak protection technology.

Real-World Impact: Reducing Strata Liability

Imagine a 50-unit strata in Coquitlam. Their water deductible was recently hiked to $50,000 after two minor claims. By investing in a building-wide retrofit with Leak Logic, they were able to present a complete risk mitigation package to their insurer.

Because they could prove 100% unit coverage, automatic shut-off capabilities, and professional monitoring, the insurer agreed to maintain a lower deductible. This saved the strata from having to pass on massive "deductible assessments" to individual owners: a move that saved the council a lot of headaches and maintained the building's property value.

For more strategies on managing these situations, you might find our guide on condo water damage strategies or advanced leak detection for insurance helpful.

Is Your Building Optimized for the Future?

Insurance companies are increasingly moving toward a "hard market" where they only want to insure the "best" risks. Proving your building’s risk mitigation isn't just about saving money today; it’s about ensuring your building remains insurable in the future.

As we look at the aging infrastructure in parts of Vancouver and the North Shore, the risk of pipe failure only increases. Being proactive with IoT water management is the most effective way to protect your budget from the unpredictability of water damage claims.

Quick Checklist for Your Insurance Presentation:

- System Specs: Note the 0.015-inch sensitivity and gold probes.

- Monitoring: Highlight the 24/7 remote monitoring and LTE redundancy.

- Certification: Include your PREVCAN and Leak Logic installation certificates.

- Auto-Shutoff: Emphasize that the water stops without human intervention.

- Freeze Protection: Mention the 5°C alerts for winter safety.

Take Control of Your Insurance Costs Today

Don’t let your next insurance renewal be a source of anxiety. You have the power to change how underwriters see your building. By partnering with Leak Logic Canada, you aren't just buying sensors; you’re investing in a professional risk-reduction partnership that protects your assets, your owners, and your bottom line.

Are you looking for a water leak detection company near me in Vancouver or the Lower Mainland? Our team at Leak Logic Canada specializes in helping property managers and Strata Councils navigate the complexities of water damage prevention and insurance compliance. Whether you're in Richmond, Burnaby, Surrey, or Coquitlam, we are here to help you safeguard your building.

Contact Leak Logic Canada today for a professional assessment and let’s get your building the protection: and the lower premiums: it deserves.

(Visualizing the ease of management through a centralized portal for property managers).

(Visualizing the ease of management through a centralized portal for property managers).

FAQ: How does leak detection lower premiums?

Insurers offer discounts or lower deductibles when you provide documented proof of a "closed-loop" system: one that detects leaks (0.015-inch sensitivity), shuts off the water automatically, and is monitored 24/7 by a professional service like Leak Logic Canada. This drastically reduces the "Maximum Foreseeable Loss" for the insurance company.